A confident young woman strides into her favorite online store to buy a new smartphone with her first salary. She adds it to her cart, and just as she’s about to check out, a prompt appears: “Need more time to pay? Split the amount into three simple installments.” With a single click, the purchase is complete — no bank visits, no paperwork, no app installations. That smooth, effortless journey she just experienced is the true essence of embedded finance — where digital payments meet customer convenience.

This is the quiet revolution driving fintech innovation, where financial services blend seamlessly into the apps and platforms people already use every day. Think of your ride-hailing app offering a digital wallet, or a healthcare platform letting you pay medical bills using instant credit. Whether it’s a retail checkout, a mobility app, or an e-commerce marketplace, embedded financial technology makes money movement as natural as the actions you’re performing — shopping, booking, or subscribing.

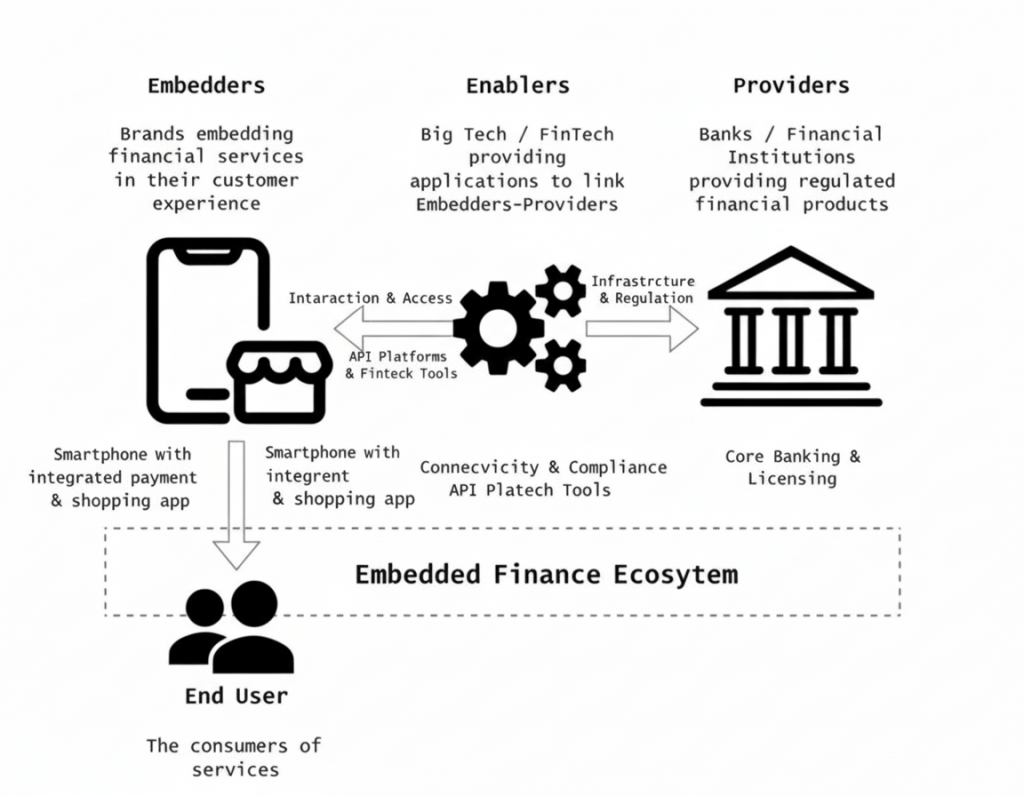

Unlike traditional banking, which asks customers to step into its world, embedded finance solutions flip the story: they bring the bank to where the customer already is. According to PwC, this model removes friction, enhances trust, and shifts financial service delivery from isolated institutions to digital ecosystems where consumers spend most of their time.

Behind this simplicity lies a powerful network. Non-financial companies are partnering with banks and fintechs — or even transforming into financial service providers themselves — to offer everything from digital payments and lending solutions to insurance and wealth management. They achieve this using APIs, white-labeled fintech platforms, and Banking-as-a-Service (BaaS) frameworks, as Alloy notes.

The result? Finance becomes invisible — embedded so deeply into digital life that it feels less like a transaction and more like a natural interaction.

This week, The People Weekly explores the growing momentum of embedded finance and its impact on evolving talent demands.

What is Embedded Finance?

Embedded finance integrates payments, lending, insurance, or investment directly into non-financial digital platforms such as e-commerce stores, mobility apps, or healthcare systems.

Examples include:

“Buy Now, Pay Later” during online shopping

In-app ride-hailing wallets

Instant insurance add-ons at checkout

This model enhances convenience, boosts customer engagement, and deeply integrates financial services into digital ecosystems. The three major categories are:

Embedded Payments

Embedded Insurance

Embedded Credit / Lending

For example, when a customer chooses a “Buy Now, Pay Later” option while shopping online or pays through a digital wallet inside a ride-hailing app, they’re experiencing embedded finance in action. By blending banking, fintech, and digital ecosystems, embedded finance delivers seamless user experiences, boosts customer engagement, and redefines how financial products are accessed and delivered in the modern economy.

Majorly there are 3 types of Embedded Finance, Embedded Payments, Embedded Insurance and Embedded Credit/ Lending.

Why Embedded Finance Is Transforming Industries, from Retail to Mobility

Embedded finance is altering the rules of customer engagement, business growth, and industry boundaries.

Here’s how:

Frictionless customer experience: For consumers, the value proposition is compelling. At the moment of decision (checkout, ride-booking, subscription, etc.) financial services are offered seamlessly e.g., “pay later”, “wallet”, “insurance add-on” rather than making the user leave the experience to go to a separate bank or lender. That convenience drives conversions, retention, and loyalty.

New revenue streams for non-financial firms: Retailers, marketplaces, mobility apps, SaaS platforms monetise deeper by offering finance whether via fee/commission, data monetisation or increased sales. Platforms can earn through:

Commissions

Higher sales via BNPL

Data-driven monetization

Capturing more of the transaction margin

Lower customer acquisition and higher stickiness: Embedding finance helps keep customers inside a brand’s ecosystem rather than losing them to external financial providers. If the retailer also offers the loan, the wallet, the insurance, the likelihood of repeated engagement increases.

Industry transformation: From retail and e-commerce to mobility (ride-hailing, logistics), insurance, automotive (connected cars + usage insurance), healthcare, travel, subscription services, embedded finance allows each of these sectors to embed value-added financial propositions that enhance core services. For mobility, for example, issuing a virtual wallet, instant ride-credit, driver financing, vehicle-insurance integrated; for retail, BNPL at checkout, merchant wallet, micro-loans to sellers.

Platform leverage and ecosystem advantage: The shift emphasises platforms rather than traditional banks. For example, a super-app or marketplace becomes the interface, and the financial service is embedded within. The “moment of need” is leveraged. This has high strategic significance.

Data and analytics opportunities: Embedded finance gives firms access to richer consumer behaviour data (purchase patterns, platform journeys) which is used for credit underwriting, risk modelling, personalised offers, and dynamic pricing. This moves the business beyond product to insight-driven financial service.

Global and Indian Market Growth

Globally, one forecast shows the embedded finance market is expected to grow from about US$146.17 billion in 2025 to US$690.39 billion by 2030 (CAGR ~36.4%). Other projections are more ambitious: e.g., the market was ~ US$111.72 billion in 2024 and projected to reach ~ US$1.732 trillion by 2034 (CAGR ~31.5%). Another research suggests by 2033, the market may reach

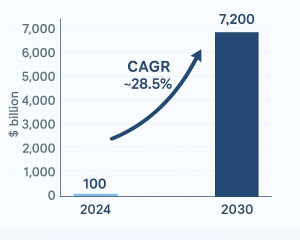

US$1,217.37 billion, from ~ US$108.55 billion in 2024 (CAGR ~28.5%). The World Economic Forum mentions a projection that the global embedded finance market may reach US$7.2 trillion by 2030.

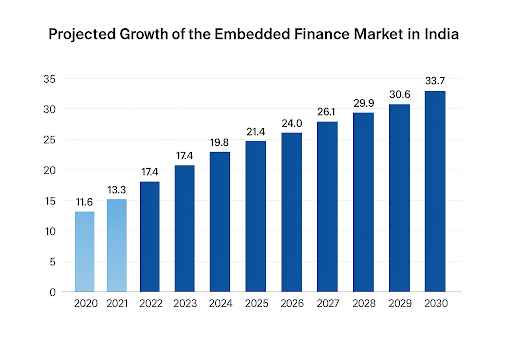

India: According to one Indian commentary, embedded finance could represent a US$ 25 billion opportunity for India’s digital and financial services platforms by 2030. Business wire has projected that “the embedded finance market in India is expected to grow by 12.4% on an annual basis to reach US$24.03 billion by 2025. The embedded finance market in the country has experienced robust growth during 2021-2025, achieving a CAGR of 17.8%. This upward trajectory is expected to continue, with the market forecast to grow at a CAGR of 8.8% from 2026 to 2030. By the end of 2030, the embedded finance market is projected to expand from its 2024 value of US$21.38 billion to approximately US$33.69 billion.”

Key Players: Fintech Startups, Traditional Banks, Tech Platforms

Fintech Infrastructure Providers

Companies like Stripe, Marqeta, and Plaid offer APIs, card issuance, and payment rails enabling embedded finance.

Traditional Banks

Banks are building BaaS capabilities and partnering with digital platforms to embed their services.

Tech Platforms & Marketplaces

E-commerce, mobility, and SaaS platforms increasingly offer lending, wallets, and insurance directly to users.

Collaboration and partnerships: The ecosystem is multiparty fintechs, banks, non-financial firms, regulators – working together to embed financial services. The value chain is shifting.

How Non-Financial Companies are Becoming Financial Service Providers

Companies evolve by:

Embedding payments, credit, wallets, or insurance into their journeys

Seeking NBFC licenses or partnering with banks (especially in India)

Using customer data to personalise financial products

Monetising new revenue lines like interchange and float income

Leveraging BaaS instead of building full banking operations

This shift blurs industry boundaries and transforms platforms into contextual financial hubs.

Top Skills & Talent Needed in Embedded Finance

The rise of embedded finance is reshaping workforce needs across industries.

1. Product Managers

Strong demand exists for PMs who understand both fintech and platform ecosystems.

2. API, Cloud & Platform Engineers

API-first architecture and cloud-native systems require highly specialised engineering talent.

3. Risk & Compliance Specialists

Platforms embedding finance need experts in:

KYC/AML

Credit risk

Fraud management

Regulatory compliance

4. Data Scientists

Behavioral, non-traditional data powers underwriting and pricing.

5. Cybersecurity & Privacy Talent

As financial data grows, so does the need for encryption, consent management, and API security specialists.

6. Ecosystem Partnership Managers

Managing multi-party relationships across banks, fintechs, and platforms is now a critical role.

The Talent Challenges Companies Face

No transition is without hurdles. In embedding finance into their offering, companies face several talent challenges:

Shortage of hybrid finance + tech professionals

Competition from Big Tech and fintechs

Difficulty attracting senior risk/compliance talent

Cultural differences between financial and non-financial teams

Need for constant upskilling in fast-changing regulatory environments

Heavy demand for cybersecurity and data governance skills

Frequently Asked Questions (FAQs)

1. What is embedded finance in simple words?

It means adding financial services like payments, loans, or insurance directly inside non-banking apps.

2. Which sectors benefit the most?

Retail, mobility, SaaS, healthcare, travel, and e-commerce.

3. Why is embedded finance growing so fast?

Because it removes friction and allows instant financial actions within apps users already trust.

4. What skills are most in demand?

API engineering, cloud systems, risk/AML, data science, cybersecurity, product management.

5. How does embedded finance affect hiring?

Companies increasingly need hybrid fintech–tech talent to build compliant, scalable financial journeys.

6. Is embedded finance relevant to India?

Absolutely — India is one of the world’s fastest-growing markets due to UPI, e-commerce, and digital adoption.

Conclusion

Embedded finance is reshaping how companies deliver value and how customers interact with financial services. As financial capabilities integrate more deeply into digital platforms, businesses must build teams with the hybrid skills needed to innovate, manage risk, and scale new financial offerings. Those who invest early in talent, technology, and ecosystem collaboration will lead the next wave of digital financial transformation.