State Of Hiring - May 2026

April suggested the market was pausing. May proved otherwise. Manufacturing hit a record high, GCCs staged a confirmed comeback, and the competition for experienced mid-senior talent is intensifying faster than most employers anticipated. Here is what the data is telling us — and what it means for your hiring strategy heading into Q1 FY 2026–27.

May 2026 — Key Signals at a Glance

State of Hiring Report · PeopleLogic Business Solutions

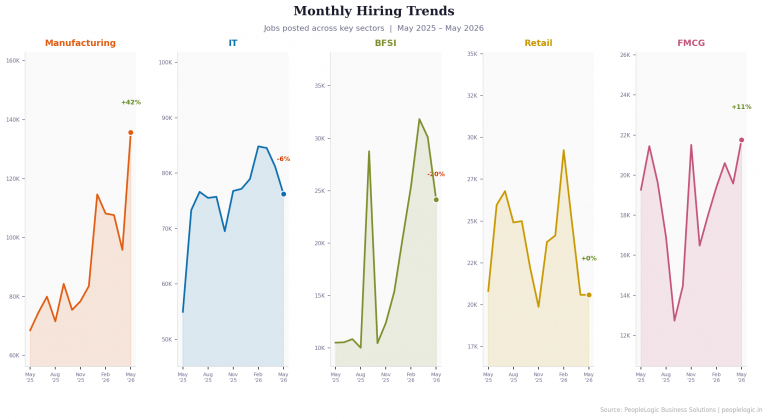

↑ 42%

Manufacturing MoM growth

Record high for FY26

Overtook IT in volume

for the first time

Overtook IT in volume

for the first time

↓ 6%

IT MoM change

Consolidation, not retreat

Demand steady in AI/ML,

Backend & ERP

Demand steady in AI/ML,

Backend & ERP

17%

GCC hiring share

↑ from 5% low in Q3

Recovery confirmed

2nd consecutive month

Recovery confirmed

2nd consecutive month

37%

IT’s share of total market

Non-IT at 63%

Tech-led market

with Non-IT breadth

Tech-led market

with Non-IT breadth

Overall Hiring Landscape

- Manufacturing overtook IT for the first time — driven by PLI investments, new plant commissions, and seasonal production ramp-ups. The gap is significant and marks a structural shift in hiring momentum.

- IT is not retreating — a 6% MoM dip looks like a correction but is consolidation at a high base. Demand continues in AI/ML, Backend, and ERP roles.

- BFSI holds structural strength — dipped from its March peak but still running at more than double its level from the same month last year.

- FMCG and Retail are steady, not exciting — both sectors hold their ground without meaningful growth or decline. Reliable pipelines, not competitive battlegrounds.

💡 The April dip was a base effect, not a demand signal.

March’s exceptional surge inflated the comparison — hiring didn’t actually slow, it normalised. Employers who read April as a pipeline-building opportunity and kept sourcing warm will find May’s recovery working in their favour. Those who paused completely are now re-entering a more competitive market.

GCCs vs IT Services vs Product Companies

- IT Services dominates at ~80% share — consistent, high-volume, strong project pipelines driving sustained demand.

- GCC recovery is confirmed, not a blip — 17% share in May, the second consecutive month of recovery after a prolonged slide to 5% in Q3.

- Product companies stay selective — ~3% share, competing on role quality and compensation rather than scale.

- The implication — GCCs and IT Services are now chasing the same 5–8 year experienced tech profiles simultaneously. The talent pool for this cohort has never been more contested.

💡 GCC recovery changes the competitive equation for everyone — not just GCC employers.

When GCCs were contracting through Q2 and Q3 of FY’26, IT Services largely had the senior tech talent pool to itself. That window has closed. The same 6–8 year Backend, AI/ML, and Architect profiles are now being pursued simultaneously by IT Services at volume and GCCs with strong brand and compensation. Expect offer-to-join ratios to fall and counter-offer rates to rise through Q1 of FY’27.

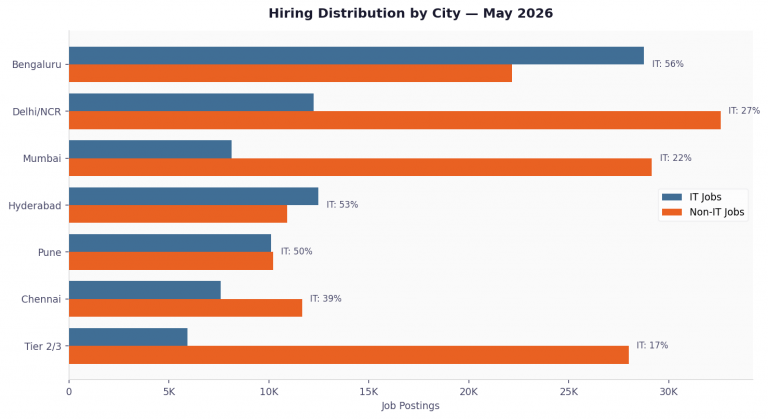

Hiring Landscape — Location Wise

- Bengaluru is the only city where IT outpaces Non-IT — 56.5% of all listings are tech roles.

- Mumbai and Delhi/NCR are Non-IT powerhouses — 78% and 73% Non-IT respectively. Large in absolute IT numbers, but Non-IT is the dominant story.

- Hyderabad and Pune are the most balanced markets — nearly equal IT and Non-IT, making them competitive for both employer types.

- Tier 2/3 cities are 82.5% Non-IT. Thin IT supply, but low competition. A genuine option for distributed hiring strategies.

- Emerging IT pockets — Kochi, Coimbatore, and Thiruvananthapuram are quietly building IT density through park and GCC corridor growth.

💡 Mumbai and Delhi/NCR play by different rules.

Each city has its own hiring logic — and national templates consistently underperform. In Mumbai, BFSI sets the compensation benchmark every employer competes against. In Delhi/NCR, talent density means candidates have more options and less urgency to move. Bengaluru’s fast, equity-driven, tech-first market is the exception, not the template. Employers who localise their approach to the city they are hiring in will always outperform those running a one-size-fits-all playbook.

Watch for in June 2026

💰

New budgets activate

Fresh IT and BFSI mandates will hit the market from mid-June.

📈

Attrition peaks

Appraisal completions drive the year’s biggest passive talent movement. Mid-senior supply tightens.

🏢

GCCs lock Q1 headcount

More competition for senior tech profiles from June onwards.

🏭

Manufacturing reality check

June data will confirm if May’s surge is structural or seasonal.

⏱️

Travel window closes

Peak season hiring fills by late June. The window is short.

💡

June will be the most competitive month for mid-senior talent this year. Move early or compete for what’s left.

Ready to build your team for Q1 FY 2026–27?

PeopleLogic works with organisations across sectors and functions — from leadership hiring to large-scale talent delivery. Tell us what you need and we will get to work.

Download the Full Report — May 2026

Talk to our team →

You May Also Like

Manufacturing

Why Global Manufacturers Are Setting Up GCCs in India — And What They’re Struggling to Find

Read more →

Hiring Strategy

Contractual Hiring Is No Longer a Backup Plan — It’s Becoming a Core Hiring Strategy

Read more →