Key Findings

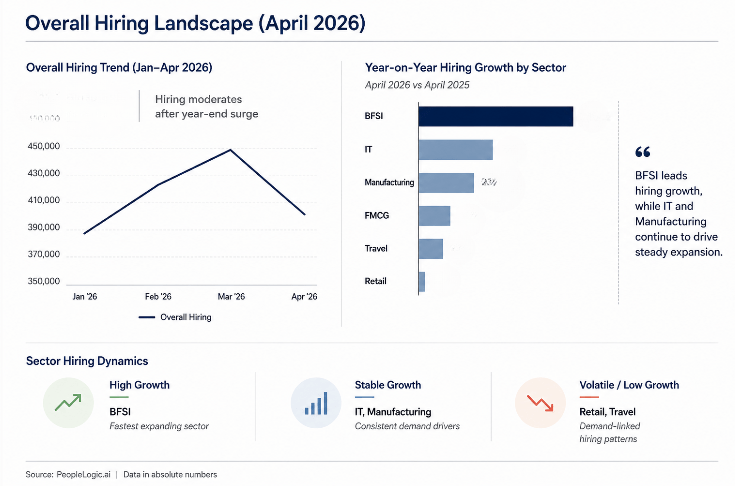

1. Hiring slows in April, but demand remains structurally strong

A ~10% MoM decline reflects a seasonal reset post financial year-end, while strong YoY growth indicates sustained underlying demand.

2. IT continues to dominate, but demand is becoming more specialised

IT accounts for the majority of hiring, with demand increasingly concentrated in AI/ML, Backend, and Full Stack roles.

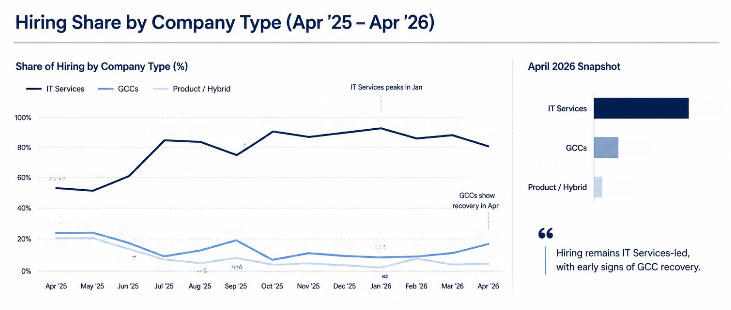

3. GCC recovery is intensifying competition for tech talent

After a period of decline, GCC hiring is rebounding, increasing competition alongside IT Services for the same talent pool.

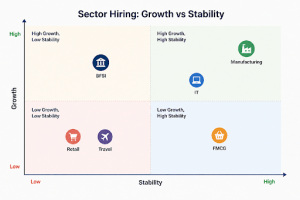

4. Hiring is increasingly sector- and role-specific

Growth is led by BFSI, Manufacturing, and IT, while consumer-facing sectors remain volatile and demand more cyclical.

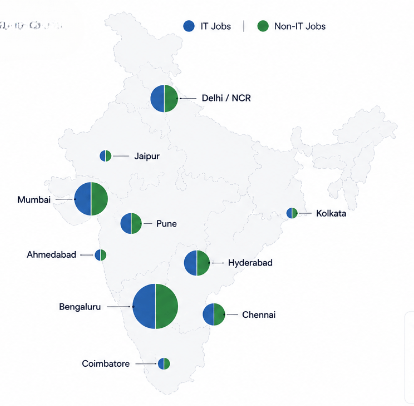

5. Location dynamics are diverging across IT and Non-IT hiring

IT hiring remains concentrated in core tech hubs, while Non-IT demand is broader and led by Mumbai and NCR, requiring location-specific hiring strategies.

Overall Hiring Landscape

Seasonal reset drives broad-based decline

Hiring dropped ~10% MoM across industries, reflecting a typical April slowdown driven by financial year reset, budget realignment, and delayed hiring decisions—not a demand collapse.

March Surge Creates a High Base Effect

The sharp increase in hiring observed in March—driven by year-end closures and budget utilisation—has amplified the perceived decline in April.

Strong Year-on-Year Growth Signals Underlying Demand

Despite the monthly dip, hiring remains significantly elevated on a year-on-year basis, indicating sustained demand across sectors.

Sector-Led Hiring Momentum Becomes More Pronounced

Growth continues to be driven by specific sectors, with BFSI, IT, and Manufacturing contributing disproportionately to overall hiring demand.

Consumer-Facing Industries Exhibit Higher Volatility

Travel and Retail sectors show sharper fluctuations, reflecting demand-linked and seasonal hiring patterns.

What This Means for Employers: Treat April as a cyclical reset while maintaining focus on critical roles amid rising talent competition.

GCCs vs IT Services vs Product Companies

IT Services dominates hiring share consistently

IT Services accounts for ~80–90% of hiring through most of the year, peaking in Jan (93%) before correcting to ~79.6% in April.

GCC hiring declined sharply, now showing recovery

GCC share dropped from ~23–24% in early months to ~5–9% in Q3/Q4, but has rebounded to 16% in April, indicating renewed hiring momentum.

Product/Hybrid hiring remains selective and niche-driven After an initial decline from ~23%, Product/Hybrid hiring has stabilised at lower levels (~3–5%), reflecting a more focused and selective hiring approach.

What this means for employers: Rising competition across IT Services and GCCs is tightening talent supply—making speed, conversion, and targeted sourcing critical for hiring success.

Hiring Landscape – Location Wise

Bengaluru is the only metro where IT dominates Non-IT — every other major city shows Non-IT demand significantly ahead, most starkly in Delhi/NCR and Mumbai .

Tier 2/3 cities are almost entirely Non-IT territory — cities like Navi Mumbai, Ahmedabad, Jaipur, and Thane have 3–5x more Non-IT openings than IT. IT employers looking to hire in these cities will face very thin talent pools and low competition from peers, but limited supply

Emerging niche IT /Non-IT clusters are visible

Thiruvananthapuram, Mysuru, and Mohali show significant IT listings — suggesting niche tech-cluster profiles. Whereas Lucknow, Faridabad, and Ghaziabad are purely Non-IT hiring markets.

Hyderabad and Pune are the most balanced metros — nearly parity between IT and Non-IT, making them competitive battlegrounds for both employer types.

What this means for employers: Hiring strategies need to be location-specific—balancing talent availability in IT-heavy hubs with broader but competitive Non-IT markets across metros and emerging cities.

Hiring Trends Across Jobs, Skills, and Experience

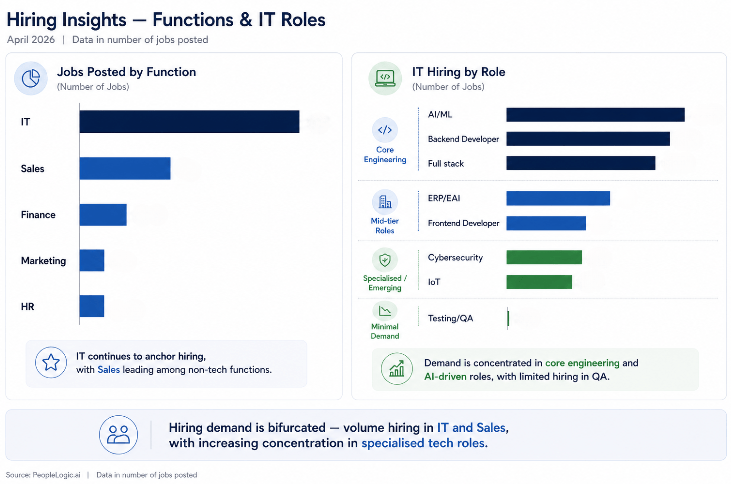

IT is not one function, it’s the market.

IT accounts for 60.5% of all postings. The next four functions combined — Sales, Finance, Marketing, HR — still don’t match IT’s volume.

AI/ML has overtaken traditional engineering as the #1 demand signal.

AI/ML edges out Backend Development and Full Stack to lead the IT role rankings. These three roles together account for over 100,000 openings — more than the entire non-IT job market.

Testing/QA has nearly vanished as a standalone role.

QA as an independent function is in structural decline — almost certainly displaced by AI-assisted testing tools and the expectation that developers own quality.

The ERP/EAI segment is larger than most expect.

Enterprise integration roles outpace Frontend Development, Cybersecurity, and IoT.

What this means for employers : Hiring success will depend on competing for core tech talent while adapting to shifts toward AI-led roles and integrated skill sets.

Methodology

We prepared this report by undertaking extensive research and study of job listings, industry reports, surveys, and expert insights. Our goal was to uncover trends and patterns in the IT hiring landscape. Additionally, we explored hiring trends across key industries like manufacturing, retail, BFSI, travel & tourism, and FMCG. We conducted a comparative analysis on a month-on-month basis to gain insights into the constantly changing IT and Non-IT hiring environment.